Top 8 GST Judgments February 2026 | ITC, Section 74, Rule 86A, Refund & Anti-Profiteering | Key Rulings for Taxpayers.

Introduction: Why February 2026 GST Rulings Matter

February 2026 has been a landmark month for GST jurisprudence in India. The GST Appellate Tribunal (GSTAT), the Supreme Court of India, and multiple High Courts have delivered rulings that significantly clarify the rights of taxpayers, the limits of departmental powers, and the procedural guardrails that must govern GST adjudication.

Whether you are a business owner, a CFO, or a taxpayer dealing with GST compliance, these rulings directly affect how you handle ITC claims, respond to show cause notices, manage refund applications, and navigate anti-profiteering allegations.

At a Glance: Summary of All 8 Judgments

The following table provides a quick reference to all eight landmark rulings covered in this article:

| No. | Case Name | Court / Forum | Key Issue | Outcome |

| 1 | Sterling & Wilson v. Commissioner, Odisha | GSTAT Delhi | GSTR-1 vs GSTR-3B Mismatch – Section 74 | Remanded to Sec. 73; not evasion |

| 2 | S.P.L. Motors v. Union of India | Punjab & Haryana HC | Rule 86A – Negative ITC Ledger Balance | Rule 86A = preventive only, not recovery |

| 3 | Union of India v. Torrent Power Ltd. | Supreme Court | Ocean Freight Refund – Unjust Enrichment | Refund to Consumer Welfare Fund |

| 4 | GSTAT Anti-Profiteering Decision | GSTAT Delhi | Base Price Hike After GST Rate Cut | Profiteering of ₹13.32 lakh confirmed |

| 5 | Raj Shekhar Pandey v. State Tax Officer | Uttarakhand HC | Portal Notice After GST Cancellation | Portal-only notice held invalid |

| 6 | Silverton Metals v. Jt. Commissioner | Calcutta HC | Extended Limitation under Section 74 | Must be allegation-specific |

| 7 | Malabar Plaza v. ASTO | Kerala HC | ITC Under Section 16(5) Relaxation | Section 16(5) overrides 16(4) |

| 8 | Raghuvansh Agro Farms v. State of UP | Allahabad HC | Section 74 Without Fraud Allegation | Proceedings quashed for lack of jurisdiction |

Judgment 1: Return Mismatch ≠ Tax Evasion (India’s First GSTAT Ruling)

| Judgment 1: Sterling & Wilson Pvt. Ltd. v. Commissioner, Odisha Commissionerate of CT & GST | |

| Citation | (2026) 39 Centax 246 (Tri.-GST-Delhi) | APL/1/PB/2026 | Decided: 11/02/2026 |

| Court / Forum | GST Appellate Tribunal (GSTAT), Delhi |

| GST Provision | Sections 73 & 74 of the CGST Act, 2017 |

| Issue | Whether mismatch between GSTR-1 and GSTR-3B automatically attracts Section 74 (fraud/suppression proceedings)? |

| Decision | The GSTAT held that a mismatch between GSTR-1 and GSTR-3B, where underlying transactions are genuine and recorded in books of accounts, cannot be treated as fraud or suppression. Section 74 proceedings were set aside and the matter was remanded for fresh consideration under Section 73 (normal limitation). The taxpayer was granted an opportunity to correct/reconcile the returns. |

| Key Takeaway | Return reconciliation differences in early GST years are common and must be examined pragmatically. Mere discrepancy is not evidence of evasion. Section 73 — not Section 74 — is the correct provision for genuine mismatches. |

Practical Example

Situation: A company filed GSTR-1 showing outward supplies of ₹50 lakhs but GSTR-3B showed ₹42 lakhs for the same period due to a software reporting error.

Before this ruling: The Department could invoke Section 74 (5-year limitation, 100% penalty) treating this as suppression.

After this ruling: The GSTAT makes clear that where the company’s books and invoices are genuine, only Section 73 proceedings (3-year limitation, 10-15% penalty) are appropriate.

Judgment 2: Rule 86A – A Preventive Tool, Not a Recovery Weapon

| Judgment 2: S.P.L. Motors Pvt. Ltd. v. Union of India | |

| Citation | (2026) 39 Centax 147 (P&H) | Punjab & Haryana High Court |

| Court / Forum | Punjab & Haryana High Court |

| GST Provision | Rule 86A of the CGST Rules, 2017 | Electronic Credit Ledger |

| Issue | Can the GST Department use Rule 86A to create a negative balance in the Electronic Credit Ledger (ECL)? |

| Decision | The High Court held that Rule 86A grants the Commissioner the power to restrict use of credit available in the ECL. However, it is a preventive power — it cannot be exercised to debit the ledger itself, thereby creating an artificial negative balance. Recovery must follow proper adjudication under Sections 73 or 74 of the CGST Act. |

| Key Takeaway | If the Department has blocked your ITC under Rule 86A and also debited your ECL creating a negative balance, this judgment is your strongest legal ground to challenge such action. |

Practical Example

Situation: GST Department suspected fake ITC claims and invoked Rule 86A, blocking ₹18 lakh in the ECL. They then debited this amount from the ECL, making the balance negative.

Legal Position After This Ruling: The debit was illegal. Rule 86A only allows freezing/blocking of available credit, not deduction. The taxpayer can approach the High Court to restore the ECL balance and require the Department to follow proper adjudication before recovery.

Judgment 3: Refund Denied Due to Unjust Enrichment – Ocean Freight Case

| Judgment 3: Union of India & Anr. v. Torrent Power Ltd. | |

| Citation | (2026) 39 Centax 265 (S.C.) | Civil Appeal No. /2026 (@SLP(C) No. 13084/2025) | 10/02/2026 |

| Court / Forum | Supreme Court of India |

| GST Provision | Section 54 of CGST Act | Unjust Enrichment Doctrine | Ocean Freight (RCM) |

| Issue | Whether refund of GST paid on ocean freight (under Reverse Charge) is available when the GST levy was subsequently held unconstitutional? |

| Decision | The Supreme Court upheld the doctrine of unjust enrichment. Since the taxpayer (importer) had already recovered the ocean freight GST cost by including it in the cost of imported goods (passed on to buyers), granting a refund would result in unjust enrichment. The refund was directed to the Consumer Welfare Fund instead. |

| Key Takeaway | Even if a tax is later struck down as unconstitutional, if you have already passed the tax burden to your customers, you cannot claim the refund yourself. Plan your pricing and documentation carefully to preserve refund rights. |

Judgment 4: Increasing Base Price on Rate Reduction Day = Profiteering

| Judgment 4: DG Anti Profiteering v. A J Enterprises | |

| Citation | (2026) 39 Centax 361 (Tri.-GST-Delhi) | NAPA/2/PB/2025 | 20/02/2026 |

| Court / Forum | GST Appellate Tribunal (GSTAT), Delhi |

| GST Provision | Section 171 of the CGST Act, 2017 (Anti-Profiteering) |

| Issue | Whether increasing base price on the same date the GST rate is reduced (from 18% to 5% for restaurants) constitutes profiteering? |

| Decision | The GSTAT confirmed profiteering. The restaurant increased its base menu prices on the exact day the GST rate was reduced from 18% to 5%, effectively neutralising the tax benefit that should have been passed to customers. Profiteering was quantified at ₹13.32 lakh. Interest was also levied and the amount was directed to be credited to Consumer Welfare Funds. |

| Key Takeaway | Every business operating in sectors where GST rates are changed must document pricing decisions carefully. Increasing MRP or base price on the day of a rate reduction — without legitimate cost justification — will attract anti-profiteering proceedings. |

Practical Example

Before Rate Cut: GST Rate 18% on base price of ₹100. Customer pays ₹118.

After Rate Cut (5%): If base price stays ₹100, customer pays ₹105 — saving ₹13.

Profiteering Scenario: Restaurant raises base price to ₹113. Customer now pays ₹113 × 1.05 = ₹118.65. The customer got no benefit. This is profiteering under Section 171.

Judgment 5: Notice Via GST Portal Invalid After Registration Cancellation

| Judgment 5: Raj Shekhar Pandey v. State Tax Officer | |

| Citation | (2026) 39 Centax 338 (Uttarakhand HC) |

| Court / Forum | Uttarakhand High Court |

| GST Provision | Section 169 of the CGST Act, 2017 (Service of Notice) |

| Issue | Whether serving a notice only through the GST portal is valid when the taxpayer’s registration has been cancelled? |

| Decision | The Uttarakhand HC held that once a GST registration is cancelled, the taxpayer cannot reasonably be expected to monitor the GST portal indefinitely. Section 169 provides multiple valid modes of service: email, speed post, registered post, publication in newspaper, etc. Relying solely on portal-based service after cancellation violates the principles of natural justice. The proceedings were set aside. |

| Key Takeaway | If you have received a GST demand order and your registration was cancelled before the notice was issued, check whether notice was properly served under Section 169. Portal-only service after cancellation is legally challengeable. |

Judgment 6: Extended Limitation Under Section 74 Must Be Allegation-Specific

| Judgment 6: Silverton Metals Pvt. Ltd. v. Joint Commissioner, Central Tax | |

| Citation | (2026) 38 Centax 218 (Cal.) | Calcutta High Court |

| Court / Forum | Calcutta High Court |

| GST Provision | Section 74 of CGST Act (Extended Limitation – 5 Years) vs. Section 73 (3 Years) |

| Issue | Can extended limitation under Section 74 be applied globally to all demands in an SCN without allegation-specific fraud statements? |

| Decision | The Calcutta HC held that invoking extended limitation under Section 74 requires the Show Cause Notice to contain specific allegations of fraud, suppression or wilful misstatement for each demand in question. A blanket invocation of Section 74 covering all demands in an SCN — without linking fraud allegations to specific transactions — is bad in law and liable to be struck down. |

| Key Takeaway | Always review the SCN carefully when Section 74 is invoked. If the fraud allegation is vague or generic (not linked to specific transactions), the jurisdictional basis for Section 74 can be challenged, which would significantly reduce the penalty exposure from 100% to 10-15%. |

Judgment 7: Section 16(5) Overrides 16(4) – ITC Allowed Despite Delay

| Judgment 7: Malabar Plaza Residency & Restaurant v. Assistant State Tax Officer (ASTO) | |

| Citation | (2026) 39 Centax 298 (Kerala HC) | Kerala High Court |

| Court / Forum | Kerala High Court |

| GST Provision | Sections 16(4) and 16(5) of CGST Act | ITC Eligibility |

| Issue | Whether ITC can be claimed under Section 16(5) for returns filed late but before the extended deadline of 30-11-2021, overriding the restriction under Section 16(4)? |

| Decision | The Kerala HC confirmed that Section 16(5) is a special statutory relaxation provision that expressly overrides the time limit under Section 16(4). Taxpayers who filed their GSTR-3B returns before 30-11-2021 for FY 2017-18 to FY 2020-21 are entitled to claim ITC even if the Section 16(4) time limit had expired. Denial of ITC solely on procedural delay grounds — when Section 16(5) applies — is illegal. |

| Key Takeaway | This is significant relief for taxpayers who were denied ITC under Section 16(4) for early GST years. If you filed returns before 30-11-2021 for the specified years and ITC was denied, this judgment supports a strong case for reclaiming that ITC. |

Judgment 8: Section 74 Cannot Be Invoked on Suspicion Alone

| Judgment 8: Raghuvansh Agro Farms Ltd. v. State of Uttar Pradesh | |

| Citation | (2026) 38 Centax 53 (All.) | Allahabad High Court |

| Court / Forum | Allahabad High Court |

| GST Provision | Section 74 of CGST Act (Fraud / Suppression / Wilful Misstatement) |

| Issue | Whether Section 74 proceedings can be initiated without clear allegations of fraud, suppression or wilful misstatement, even where transactions are supported by documents? |

| Decision | The Allahabad HC quashed Section 74 proceedings initiated against the taxpayer. The taxpayer’s transactions were supported by tax invoices, e-way bills, and corresponding bank entries. The HC held that suspicion, however strong, cannot substitute for specific fraud allegations. The Department had not established any case of fraud. Section 74 proceedings were held to be without jurisdiction. |

| Key Takeaway | If you face Section 74 proceedings but your transactions are supported by invoices, e-way bills, and bank records, and the SCN does not contain specific fraud allegations, this ruling provides strong precedent to challenge the proceedings at an early stage. |

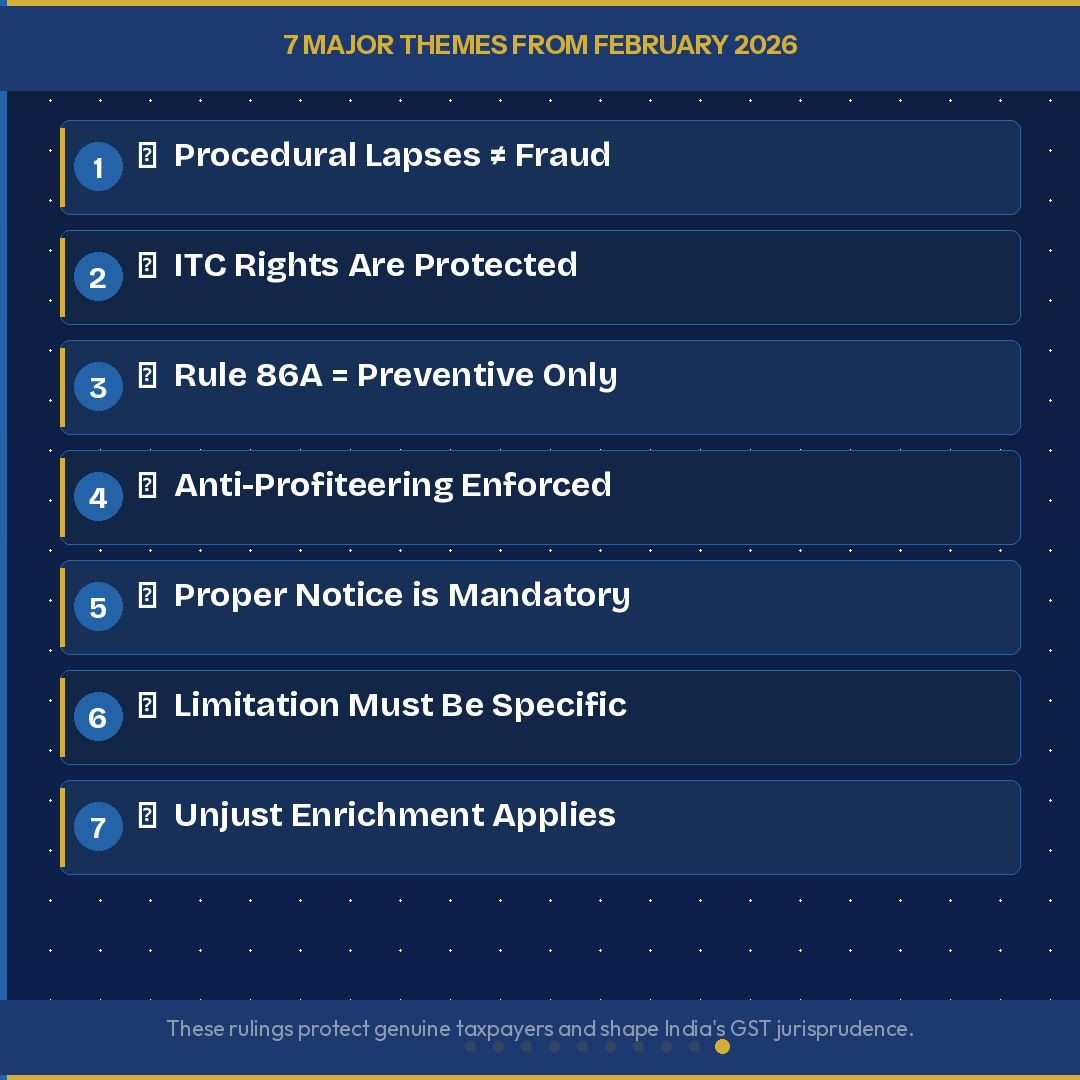

Major Themes Emerging from February 2026 GST Rulings

These eight rulings are not isolated decisions. Together, they reflect seven clear themes that are shaping the future of GST jurisprudence in India:

| Theme | Insight |

| ⚖ Procedural Fairness | Courts have repeatedly held that procedural lapses cannot be equated to fraud or tax evasion. GST administration must be based on substance over form. |

| 🛡 Protection of ITC Rights | Section 16(5) offers significant protection to taxpayers. Courts are actively preventing arbitrary denial of ITC where genuine transactions exist. |

| 🔍 Rule 86A – Preventive, Not Punitive | Rule 86A is being interpreted narrowly. It can freeze credit but cannot create artificial liabilities. This is a significant relief for compliant taxpayers. |

| 💰 Consumer Protection via Anti-Profiteering | Anti-profiteering provisions under Section 171 are being strictly enforced. Base price manipulation after GST rate changes will attract penalties. |

| 📬 Proper Notice Service is Non-Negotiable | Serving notice only on the GST portal, especially after registration cancellation, is no longer acceptable. Proper modes under Section 169 must be followed. |

| ⏱ Limitation Must Be Allegation-Specific | Extended limitation (5 years) under Section 74 requires specific fraud allegations. Courts are rejecting blanket application of extended limitation. |

| 🚫 Unjust Enrichment Principle | Refunds are not automatic even when taxes are struck down. If the burden was passed to consumers, refund goes to Consumer Welfare Fund. |

Frequently Asked Questions (FAQs)

Based on the rulings discussed, here are answers to the most common questions taxpayers and businesses ask:

| Frequently Asked Questions (FAQs) on February 2026 GST Judgments |

| Q1. Can a mismatch between GSTR-1 and GSTR-3B lead to Section 74 proceedings? |

| Not automatically. As per the GSTAT ruling in Sterling & Wilson, return mismatches arising from genuine transactions and procedural lapses cannot be treated as fraud or suppression. Section 73 proceedings (not Section 74) would be the appropriate route. |

| Q2. Can the GST Department use Rule 86A to create a negative balance in the Electronic Credit Ledger? |

| No. The Punjab & Haryana HC clarified that Rule 86A is a preventive tool to freeze available credit. It cannot be used to debit the ledger and create an artificial negative balance. Recovery must follow adjudication under Sections 73/74. |

| Q3. Is a GST refund always available when a tax is held unconstitutional? |

| Not necessarily. The Supreme Court in Union of India v. Torrent Power held that if the taxpayer has already passed on the tax burden to consumers, the doctrine of unjust enrichment applies. Refund in such cases goes to the Consumer Welfare Fund. |

| Q4. What happens if a supplier increases base prices the same day GST rate is reduced? |

| This constitutes profiteering under Section 171 of the CGST Act. The GSTAT confirmed that the full benefit of tax rate reduction must be passed on to the consumer. Any base price increase to absorb the benefit is treated as profiteering. |

| Q5. Is a notice served only on the GST portal valid after registration cancellation? |

| No. The Uttarakhand HC held that a taxpayer cannot be expected to monitor a cancelled registration’s portal account indefinitely. The Department must use proper service modes under Section 169 (like email, registered post, etc.). |

| Q6. Can extended limitation under Section 74 be applied to all demands in an SCN? |

| No. The Calcutta HC held that extended limitation must be allegation-specific. Unless each demand is supported by specific fraud or suppression allegations, extended limitation cannot be invoked across the board. |

| Q7. Does Section 16(5) override the time limit under Section 16(4) for claiming ITC? |

| Yes. The Kerala HC confirmed that Section 16(5) is a special relaxation provision that overrides Section 16(4). Taxpayers who filed returns before 30-11-2021 for the specified period can claim ITC even if the regular time limit had expired. |

| Q8. Can the Department initiate Section 74 proceedings merely on suspicion? |

| No. The Allahabad HC firmly held that Section 74 requires clear allegations of fraud, suppression, or wilful misstatement. Genuine transactions supported by invoices, e-way bills, and bank records cannot be subjected to Section 74 proceedings based on mere suspicion. |

Compliance Checklist: What Taxpayers Should Do Now

| S.No | Action Item | Related Judgment |

| 1 | Reconcile GSTR-1 and GSTR-3B for all open periods. If mismatches exist, prepare reconciliation statements and explanatory notes before any SCN arrives. | Judgment 1 |

| 2 | If Rule 86A has been invoked and your ECL shows a negative balance, consult your CA immediately — the debit may be legally unjustified. | Judgment 2 |

| 3 | For refund applications, document whether GST cost was passed to buyers or absorbed. This determines unjust enrichment applicability. | Judgment 3 |

| 4 | If your sector saw a GST rate change, review your pricing history. Maintain MRP change documentation with cost justification to defend against anti-profiteering. | Judgment 4 |

| 5 | If your GST registration is cancelled and you receive a portal notice, verify compliance with Section 169 before accepting any demand as valid. | Judgment 5 |

| 6 | For every Section 74 SCN, check whether fraud allegations are allegation-specific or generic. Generic invocation of Section 74 is a strong ground for challenge. | Judgment 6 |

| 7 | If ITC was denied under Section 16(4) for FY 2017-21 and you filed GSTR-3B before 30-11-2021, file for reconsideration citing Section 16(5). | Judgment 7 |

| 8 | If Section 74 proceedings are initiated against genuinely documented transactions, gather all invoices, e-way bills, and bank records to establish there is no fraud. | Judgment 8 |

Conclusion

February 2026 has delivered a clear message from India’s courts and tribunals: GST adjudication must be grounded in evidence, procedural fairness, and the rule of law. Procedural lapses alone are not fraud. ITC rights must be protected. Anti-profiteering principles exist to protect consumers, not to create arbitrary business obligations. Notices must be properly served. Limitation provisions must be correctly applied.

For taxpayers and businesses, these eight rulings are powerful tools in any GST compliance and litigation strategy. For any specific queries regarding your GST matters, it is advisable to consult a qualified Chartered Accountant.

Disclaimer: This article is prepared for educational and informational purposes only. It does not constitute legal or tax advice. Readers are advised to consult a qualified Chartered Accountant or tax professional for advice specific to their circumstances.