GST on Charitable Organisations: What Every Trust & NGO Must Know.

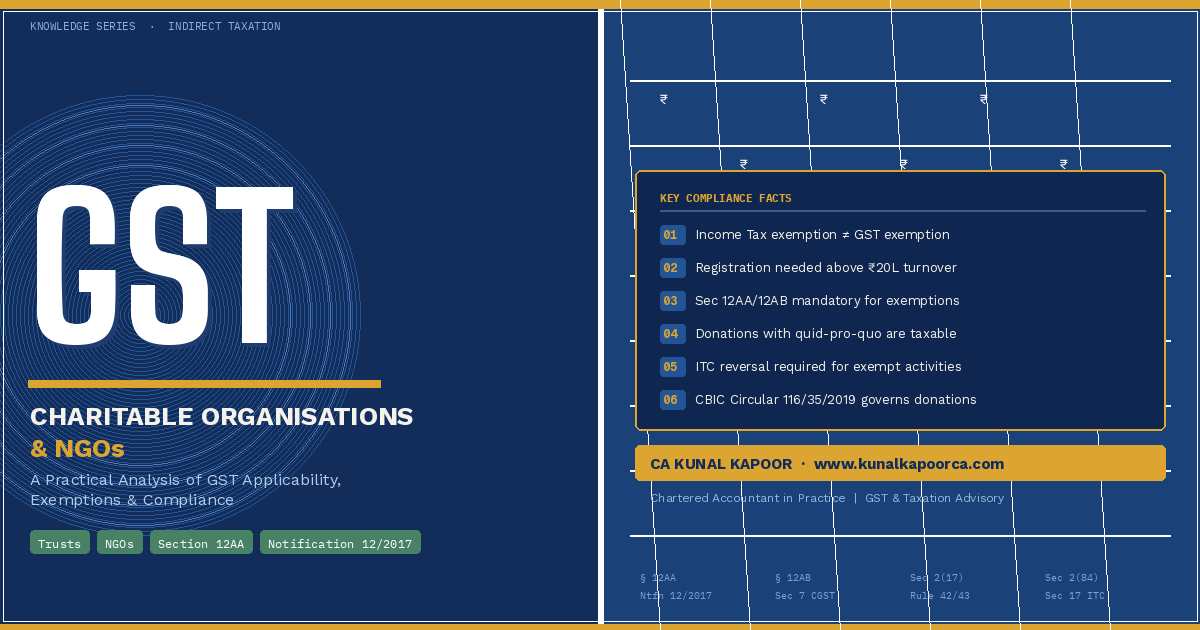

Charitable organisations — trusts, societies, and NGOs — occupy a unique and vital space in our social fabric. Many of them rightly enjoy exemptions under the Income-tax Act, 1961. However, a common and costly misconception is that an Income Tax exemption automatically extends to Goods and Services Tax (GST) as well. It does not. GST operates on an entirely independent framework, and the two laws must be evaluated separately. This article walks through the key GST implications for charitable organisations — covering registration, taxability of activities, donations, exemptions, and more — in a practical, easy-to-understand manner. https://incometaxindia.gov.in/

1. Are Charitable Organisations Recognised Under GST?

Yes. Under Section 2(84) of the CGST Act, 2017, the term ‘person’ is defined broadly to include trusts, societies, associations, and other artificial juridical persons. This means that charitable organisations are fully recognised as taxable persons under GST — just like any other business entity.

| Key Takeaway: Being a charitable organisation does not, by itself, exclude you from the GST framework. The question is whether your specific activities attract GST. |

2. When Does GST Actually Apply to an NGO or Trust?

For GST to be applicable to any activity of a charitable organisation, three conditions must be satisfied simultaneously:

Supply: Section 7 of the CGST Act defines supply very broadly — it includes sale, transfer, barter, exchange, licence, rental, lease, or disposal of goods or services. Most activities of an NGO could potentially fall within this definition.

Business Activity: Under Section 2(17), ‘business’ includes any trade, commerce, profession, or similar activity — whether or not it is carried on for profit. This is crucial: even welfare-oriented work can qualify as a ‘business’ under GST.

Consideration: Any payment received — even a token amount or concessional price — constitutes ‘consideration’. However, completely free distributions with no payment involved generally fall outside the ambit of GST.

| Example: If a trust distributes meals absolutely free of charge, GST does not apply. However, if it charges even a nominal price (say ₹10 per meal), that constitutes consideration and the supply becomes taxable — unless specifically exempted. |

3. Exemptions Available Under GST: The Specific Conditions

GST law does provide limited and specific exemptions to charitable organisations under Notification No. 12/2017 – Central Tax (Rate). However, two mandatory conditions must both be satisfied:https://cbic-gst.gov.in/

- The organisation must be registered under Section 12AA or 12AB of the Income-tax Act, 1961.

- The services must qualify as ‘charitable activities’ as defined in the notification.

What Counts as ‘Charitable Activities’ for GST?

The term is specifically defined and includes services related to:

- Public health — including diagnosis, treatment, and care of persons

- Advancement of religion, spirituality, or yoga

- Education or skill development programmes specifically for:

- Abandoned, orphaned, or homeless children

- Physically or mentally abused persons

- Prisoners

- Persons aged 65 years or above residing in rural areas

- Preservation of environment (including watershed, forests, and wildlife)

| Important: General education or training programmes for the public, corporate employees, or professionals do not fall within this definition. Such activities remain taxable under GST. |

4. Educational Institutions: A Special Category

If a charitable trust runs a recognised educational institution — a school, college, or approved vocational training institute — the GST treatment is even more favourable. Services provided to students, faculty, and staff by such institutions are fully exempt under Entry 66 of Notification No. 12/2017-CTR.

This exemption applies independently of whether the trust holds a 12AA or 12AB registration. It is a standalone exemption for educational institutions.

Additionally, certain services received by such institutions — such as catering, security, or housekeeping — are also exempt under specific conditions laid down in the same notification.

| Taxable Activities in Education: Skill development courses for working professionals, private tuitions, and courses leading to unrecognised degrees remain taxable under GST — even if run by a registered trust. |

5. GST Registration: Is Your Organisation Required to Register?

A charitable organisation must register for GST if any of the following conditions apply:

- Its aggregate turnover from taxable supplies exceeds the threshold limit (₹40 lakhs for goods; ₹20 lakhs for services in most states — ₹10 lakhs in certain special category states).

- It makes inter-state taxable supplies, irrespective of turnover.

- It is liable to pay GST under the Reverse Charge Mechanism (RCM).

An important point for threshold calculation: both exempt and taxable supplies are aggregated for computing turnover. However, organisations exclusively engaged in making exempt supplies are not required to register solely on account of RCM liability — Section 23 provides an override in such cases.

6. Taxability of Donations: Drawing the Critical Line

This is one of the most common areas of confusion for charitable organisations. The taxability of a donation depends entirely on whether the donor receives any benefit in return.https://taxinformation.cbic.gov.in/

| Type of Donation | GST Applicable? | Example |

| Pure donation — no obligation, no benefit to donor | No | Donation for free education of underprivileged children |

| Donation with display of donor name as gratitude (no business promotion) | No | ‘Donated by Mr. X’ on a hospital room door |

| Donation where donor’s brand/logo is displayed or promoted | Yes | ‘Best Tea by X Tea Co.’ with logo — amounts to sponsorship |

| Sponsorship arrangements with naming rights, brand exposure, or promotion | Yes | Event naming rights, building naming rights |

| Training conducted for donor’s employees as part of a CSR arrangement | Yes | Corporate-funded skill workshops for their own workforce |

| CBIC Clarification: Circular No. 116/35/2019-GST dated 11 October 2019 provides helpful clarity on this. The key test is whether the display of a donor’s name serves as genuine gratitude or functions as commercial advertising. The same principles apply to CSR donations. |

7. Concessional Supplies: How Is GST Calculated?

Where a trust supplies goods or services at a concessional rate — and the supply is not specifically exempt — GST applies on the actual consideration received, not on the market value.

| Example: A trust sells notebooks worth ₹100 in the market at ₹20 to beneficiaries. If the supply is taxable, GST will be calculated on ₹20 (the actual price charged), not on ₹100. Market value is irrelevant unless the transaction involves related parties or distinct persons (such as branches). |

8. Input Tax Credit (ITC): What Can Be Claimed?

For organisations that undertake both taxable and exempt activities, the ITC position requires careful management:

- ITC attributable to taxable supplies is available and can be claimed.

- ITC attributable to exempt or non-taxable supplies must be reversed as per Section 17 of the CGST Act, read with Rules 42 and 43 of the CGST Rules.

Proper allocation of input credits and timely reversals are essential to avoid interest and penalty exposure during GST audits.

9. Reverse Charge on Imported Services

NGOs registered under Section 12AA or 12AB that import services from abroad for carrying out charitable activities are exempt from IGST under the Reverse Charge Mechanism, as per Entry 10 of Notification No. 9/2017 – Integrated Tax (Rate). https://cbic-gst.gov.in/

However, this exemption is specific to services used for charitable activities. If the same organisation imports services for administrative, commercial, or non-charitable purposes (for example, foreign software for accounting), GST under RCM becomes payable. Additionally, online information and database access services (OIDAR) and transportation of goods by vessel from outside India remain taxable under RCM regardless.

10. Rent from Religious or Charitable Properties

Rental income from premises owned by religious or charitable trusts is exempt only if the following conditions are met:

- The premises must be a religious place meant for use by the general public.

- Daily rent for rooms must be below ₹1,000.

- Daily rent for community halls, open areas, or kalyanamandapams must be below ₹10,000.

- Monthly rent for shops or other spaces on the premises must be below ₹10,000.

Rents exceeding these limits attract GST even for charitable or religious trusts.

Conclusion: GST Compliance Cannot Be Assumed — It Must Be Assessed

For charitable organisations, GST compliance requires a careful, activity-by-activity evaluation. The nature of each supply, the presence or absence of consideration, and the applicability of specific exemptions must all be analysed individually.

Relying solely on Income Tax exemption status, or assuming that all activities of a registered trust are automatically exempt from GST, is a common error that can lead to significant tax exposure, interest, and penalties.

Key action points for trustees, governing boards, and management committees:

- Assess whether your organisation meets the GST registration threshold.

- Map each activity to determine taxability and applicable exemptions.

- Review all donation and sponsorship arrangements to classify them correctly.

- Ensure timely ITC reversals for exempt activities.

- Review rental income from trust properties against prescribed thresholds.

| Disclaimer: This article is intended for general educational purposes only and does not constitute legal or tax advice. The laws, notifications, and circulars referenced are subject to change. Charitable organisations should consult a qualified Chartered Accountant before taking any action based on the information contained herein. |