Convert Partnership to Private Limited via Business Transfer.

Are you looking to scale your existing partnership firm by transitioning into a corporate structure? You can convert your partnership to a Private Limited company through the Business Transfer route to enjoy benefits like limited liability and easier fundraising. This guide explains the step-by-step process, tax implications, and legal requirements specifically for business owners, startups, and expanding entrepreneurs in India who want a seamless transition.

Understanding the Business Transfer Route for Conversion

When we talk about moving from a traditional partnership to a corporate entity, the “Business Transfer” route—often executed as a Slump Sale—is a popular choice. Unlike the “Part I” conversion under the Companies Act 2013, which is a statutory conversion, the business transfer involves a new company “buying” the undertaking of the firm.

What is a Business Transfer Agreement?

A Business Transfer Agreement (BTA) is a legal contract where the partnership firm transfers its assets, liabilities, and “going concern” status to a newly incorporated Private Limited company. This is usually done for a lump-sum consideration without assigning individual values to each asset. Defining this clearly is vital to ensure that the transfer qualifies for tax neutral status under the Income Tax Act.

Legal Entity Status and Continuity

In this route, the partnership firm and the Private Limited company are treated as two distinct legal entities. The company is first incorporated, and then it “acquires” the business of the firm. You must ensure that the object clause of the new company specifically allows for the acquisition of the existing partnership business to maintain operational continuity.

Key Differences: Partnership vs. Private Limited Company

Before proceeding with the conversion, it is essential to understand why this shift is beneficial for your growth. While a partnership is easy to manage, a Private Limited company offers a more robust framework for attracting investors and protecting personal wealth.

Table 1: Comparison between Partnership Firm and Private Limited Company

| Feature | Partnership Firm | Private Limited Company |

| Liability | Unlimited Personal Liability | Limited to Share Capital |

| Governance | Partnership Act, 1932 | Companies Act, 2013 |

| Fundraising | Limited to Partners | Can Issue Equity/VC Funding |

| Compliance | Minimal | Annual ROC Filings Mandatory |

| Tax Rate | Flat 30% + Surcharge/Cess | 15% to 25% (Subject to conditions) |

Real-World Example: Scaling a Manufacturing Unit

Consider “Vikas Enterprises,” a partnership firm in Pune manufacturing auto components. The partners, Vikas and Rohan, wanted to pitch for a large international contract that required a corporate structure. They incorporated “Vikas Precision Components Pvt Ltd” and transferred the firm’s entire business (assets worth ₹50 Lakhs and liabilities of ₹10 Lakhs) via the business transfer route. By doing this, they successfully secured the contract and limited their personal risk, which was previously tied to their personal assets.

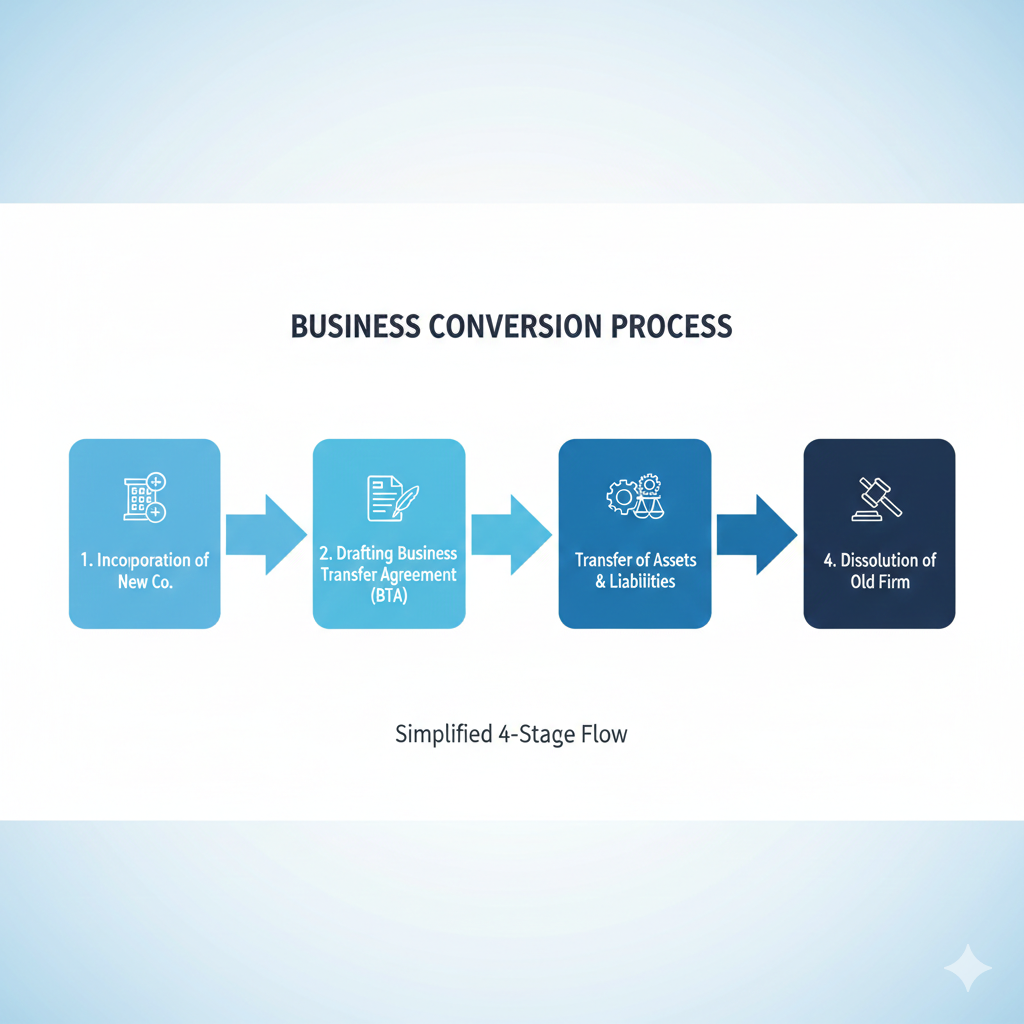

Step-by-Step Process for Conversion

The conversion through the business transfer route requires careful synchronization between the Ministry of Corporate Affairs (MCA) and the Income Tax Department.

- Incorporate the Private Limited Company: The partners must first incorporate a new company with at least two directors and two shareholders. https://www.mca.gov.in/

- Draft the Business Transfer Agreement: Prepare a BTA that specifies the lump-sum consideration and ensures all assets/liabilities are included.

- Compliance with Section 47(xiii): To avoid Capital Gains tax, ensure all partners become shareholders and their shareholding remains at least 50% for 5 years.https://www.incometax.gov.in/

- Update GST and Bank Records: Since the PAN changes, you must apply for a new GST registration and transfer the Input Tax Credit (ITC) using Form GST ITC-02.https://www.gst.gov.in/

- Transfer of Licenses: All professional licenses, brand names, and trademarks must be legally assigned to the new company.

- Dissolution of Partnership: Once the transfer is complete, the old partnership deed is cancelled, and the firm is formally dissolved.

Common Mistakes to Avoid

- Valuing assets individually during the transfer, which might trigger unwanted tax liabilities.

- Failing to transfer the GST Input Tax Credit through the proper electronic filing.

- Changing the shareholding pattern too quickly (within 5 years), leading to a withdrawal of tax exemptions.

Key Takeaways

- The business transfer route allows for a clean transition of a “going concern” business to a corporate structure.

- Limited liability protection is the biggest advantage for partners moving to a Private Limited setup.

- Tax neutrality can be achieved if the conditions under Section 47(xiii) of the Income Tax Act are strictly followed.

- A new PAN and GSTIN are mandatory, as the company is a separate legal entity from the firm.

Frequently Asked Questions

Is it mandatory to have a Business Transfer Agreement?

Yes, a BTA is a vital legal document that proves the sale of the business from the firm to the company. It serves as the primary evidence for the transfer of assets, liabilities, and the “going concern” nature of the business for both tax and regulatory purposes.

What is the minimum number of shareholders required for the new company?

To incorporate a Private Limited company in India, you need a minimum of two shareholders and two directors. Usually, the existing partners of the firm take up these roles to maintain continuity and comply with tax-saving provisions.

What happens to the existing GST registration of the partnership?

Since the Private Limited company is a new legal entity with a new PAN, the old GST registration of the partnership must be cancelled. However, the accumulated Input Tax Credit (ITC) can be transferred to the new company by filing Form GST ITC-02.

Can I convert my partnership if I have outstanding bank loans?

Yes, but you must obtain a No Objection Certificate (NOC) from your lending bank. The bank will typically require a fresh loan agreement in the name of the new Private Limited company and may ask for personal guarantees from the directors.

What are the tax implications if I don’t follow Section 47(xiii)?

If the conditions for tax-neutral conversion are not met, the transfer will be treated as a “Slump Sale” under Section 50B. This could result in heavy Capital Gains tax on the difference between the sale consideration and the net worth of the firm.

Disclaimer

This blog is intended for general informational and educational purposes only. It does not constitute professional legal, tax, or financial advice. Tax laws, GST provisions, and corporate regulations are subject to frequent amendments. The information provided is based on laws and circulars prevailing at the time of writing. Readers are strongly advised to consult a qualified Chartered Accountant or tax professional before making any financial, tax, or compliance-related decisions. CA Kunal Kapoor & Associates shall not be held responsible for any loss, liability, or consequences arising from reliance on the information contained in this blog.

Connect With CA Kunal Kapoor

Have questions about converting your partnership to a Private Limited company? CA Kunal Kapoor provides professional guidance on business restructuring and MCA compliance for business owners, startups, HNIs, and NRIs across India. Book a consultation to discuss your specific situation and get expert advice tailored to your needs.