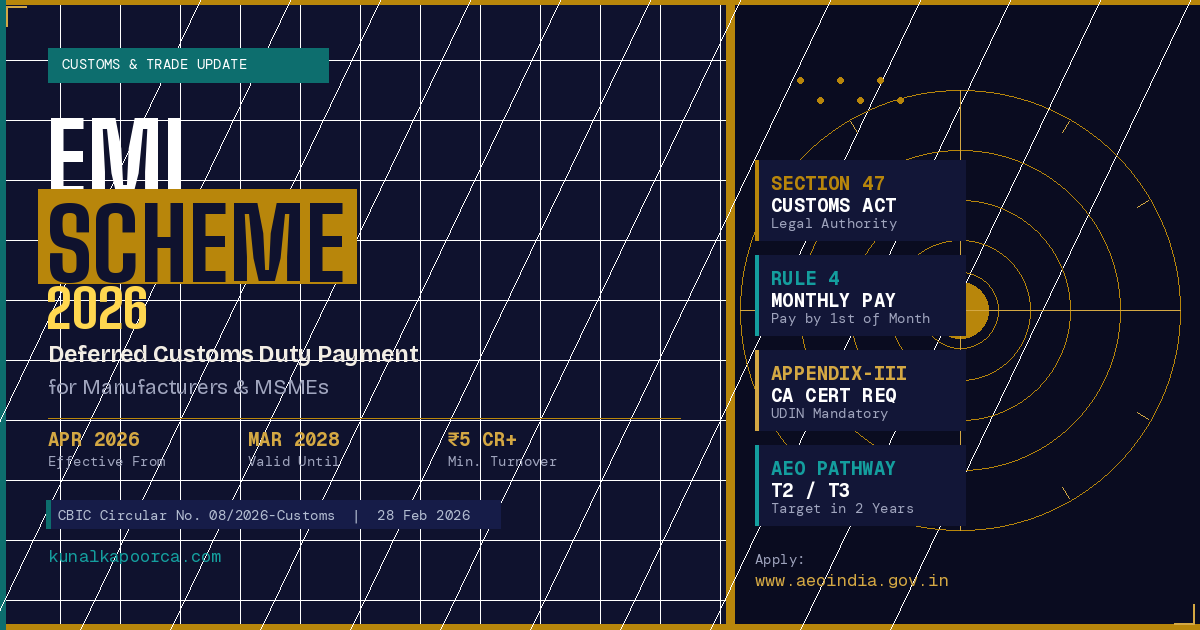

EMI Scheme 2026: Deferred Customs Duty for Manufacturers.

The EMI Scheme 2026:

Deferred Customs Duty Payment

for Manufacturers & MSMEs

CBIC’s Eligible Manufacturer Importer (EMI) Scheme allows approved manufacturers to clear imported goods without paying customs duty upfront — and settle it monthly instead. Here’s everything you need to know.

📄 Circular No. 08/2026-Customs dated 28 February 2026 — CBIC (Full Text PDF)

📢 PIB Press Release — Ministry of Finance

🌐 AEO India Portal — www.aeoindia.gov.in (Apply under tab: “Eligible Manufacturer Importer”)

📋 Notification No. 12/2026-Customs (N.T.) dated 1 February 2026 — Legal basis

SECTION 01What is the EMI Scheme? The Big Picture

Every importer in India knows this pain: before your consignment is released from port, you must pay the full customs duty — sometimes running into lakhs or crores — upfront. This locks up working capital at the worst possible time.

The Eligible Manufacturer Importer (EMI) Scheme, announced in Union Budget 2026–27 and operationalised by CBIC Circular No. 08/2026-Customs dated 28 February 2026, changes this for qualifying manufacturers. Under the scheme, approved manufacturers can clear their imported goods first and pay the customs duty later — on a convenient monthly schedule.

The scheme draws its legal authority from the proviso to Section 47(1) of the Customs Act, 1962 and is governed by the Deferred Payment of Import Duty Rules, 2016 (as amended).

SECTION 02Who Can Apply? — Eligibility Criteria in Detail

The scheme is designed as a trust-based facilitation. CBIC has laid out 15 specific conditions that an applicant must satisfy. Here is a complete breakdown:

| # | Eligibility Condition | Requirement | MSME Relaxation? |

|---|---|---|---|

| 1 | Manufacturer & Importer Status | Must be a manufacturer (u/s 2(72) CGST Act) or send inputs to job worker u/s 143 CGST | No |

| 2 | Valid IEC | Active Importer Exporter Code (DGFT) | No |

| 3 | Customs Footprint (EXIM filings) | Minimum 25 BEs/SBs in previous financial year | Yes — Only 10 for MSMEs |

| 4 | GST Registration | At least one active GSTIN under CGST/SGST Act | No |

| 5 | Manufacturing Declaration in GSTIN | REG-01 (Col 16(d) or 20(d)) must show “factory/manufacturing” | No |

| 6 | Annual Turnover | Aggregate turnover of all GSTINs (same PAN) > ₹5 Crore in last FY | No |

| 7 | Business Continuity | Business active for at least 2 financial years before application date | No |

| 8 | GST Return Compliance | All pending GSTR-3B returns must be filed for all active GSTINs as on application date | No |

| 9 | No GST Collected but Not Deposited | No instances of tax collected from customers but not deposited with Government | No |

| 10 | No Central Excise / Service Tax Arrears | No instances of duty collected but not deposited under erstwhile laws | No |

| 11 | Financial Solvency | Financially solvent for last 2 years. No insolvency / liquidation. Positive net worth & net current assets required. CA Certificate (with UDIN) mandatory. | No |

| 12 | No Arrest / Conviction | No arrest or conviction of applicant / directors / partners under Customs, Central Excise, GST or other tax laws | No |

| 13 | No Pending Prosecution | No pending prosecution proceedings under relevant tax statutes | No |

| 14 | No Past Rejection (False Info) | Earlier EMI application must not have been rejected for submitting false/forged documents | No |

| 15 | No Past Suspension (False Info) | Earlier EMI approval must not have been suspended on grounds of false information | No |

SECTION 03How to Apply — Step-by-Step Process

-

Register on the AEO India Portal

Visit www.aeoindia.gov.in and click on the tab “Eligible Manufacturer Importer”. Applications are open from 1 March 2026.

-

Fill Application Form (Appendix-I)

Complete all parts — Part A (General), Part B (if manufacturer) or Part C (if job-work route), Part D (legal & financial compliance), and Part E-G (previous applications, contact details, declarations).

-

Upload Required Documents (Appendix-II)

IEC copy, PAN, all GST certificates, UDYAM certificate (if MSME), GST ITC-04 (if applicable), GSTR-9C, CA Solvency Certificate with UDIN, last 2 years audited financials, property documents.

-

Directorate of International Customs (DIC) Review

DIC, CBIC will scrutinise the application. On approval, the system is updated to enable deferred payment — no further action required by the applicant.

-

ICEGATE Registration for Nodal Person

The EMI appoints a nodal person who registers on ICEGATE. This person will authenticate all customs transactions via OTP on behalf of the EMI.

-

Use Flag “D” on Bills of Entry

When filing a Bill of Entry under deferred payment, select “D” in the Payment Method column and complete OTP authentication through ICEGATE. Clearance is granted only after this authentication.

SECTION 04When Must You Pay? — Payment Due Dates

| Period of Import / BE Clearance | Duty Payment Due Date | Early Payment Allowed? |

|---|---|---|

| 1st to last day of any month (other than March) | 1st of the following month | Yes |

| 1st to 31st March | 31st March | Yes |

Source: Rule 4 of the Deferred Payment of Import Duty Rules, 2016 — as cited in para 7 of Circular No. 08/2026-Customs.

SECTION 05Worked Examples — Understand with Real Scenarios

Example 1: A Textile Manufacturer Importing Fabric (Non-March Month)

Scenario: M/s Weave India Pvt. Ltd. is an approved EMI. It imports synthetic fabric from China. Bills of Entry are filed and goods are cleared on 15 July 2026. Customs duty assessed = ₹8,50,000.

- Under traditional process: ₹8,50,000 must be paid before goods are released.

- Under EMI Scheme: Goods cleared on 15 July 2026. Duty of ₹8,50,000 due by 1 August 2026.

- Benefit: 16 days of additional working capital — the funds stay in the business during peak production.

Example 2: An MSME Auto Parts Maker Importing Components (March)

Scenario: M/s Precision Auto Components (an MSME) imports steel parts on 20 March 2027. Customs duty = ₹2,30,000.

- Under traditional process: ₹2,30,000 paid on the day of clearance.

- Under EMI Scheme: Goods cleared on 20 March 2027. Duty due by 31 March 2027.

- Benefit: 11 extra days to arrange funds — critical for MSMEs managing quarterly collections.

Example 3: Job-Work Route — A Garment Exporter Sending Fabric to a Job Worker

Scenario: M/s Fashion Forward Exports imports fabric but sends it to a job worker under Section 143 of CGST Act (without payment of tax). They are not manufacturers themselves.

- They are eligible for EMI, provided:

- Their GSTIN has filed last two half-yearly GSTR ITC-04 returns.

- The job worker has an active GSTIN declaring “factory/manufacturing” in REG-01.

- All other eligibility criteria (turnover, solvency etc.) are met.

SECTION 06The AEO Pathway — What Comes After EMI?

The EMI Scheme is explicitly designed as a stepping stone, not a permanent facility. CBIC expects approved EMIs to progressively obtain AEO-T2 or AEO-T3 status within the scheme’s validity period (by 31 March 2028).

| Stage | Who | Benefits |

|---|---|---|

| EMI Scheme | Trusted manufacturers meeting basic compliance threshold | Deferred customs duty payment (monthly), faster clearance |

| AEO-T1 | Existing AEO-T1 entities (also eligible for EMI) | Priority examination, reduced examinations, self-sealing |

| AEO-T2 (target) | Entities progressing from EMI/AEO-T1 | Deferred duty (existing), enhanced facilitation, fast-track clearance |

| AEO-T3 (target) | Highest-compliance exporters/importers | Maximum facilitation, priority treatment, dedicated client manager |

SECTION 07The CA Certificate — A Key Requirement

One of the most important documents in the EMI application is the Chartered Accountant Certificate (Appendix-III). This certificate must be issued on the CA Firm’s letterhead and must carry a valid UDIN (Unique Document Identification Number).

The certificate must cover the following for the last two financial years:

| Item Certified | What It Covers |

|---|---|

| Financial Summary | Total assets, fixed assets, liabilities, net worth, current assets & liabilities, turnover, current ratio, debt-equity ratio |

| Positive Net Worth | Total assets exceed total liabilities; capital + reserves are positive |

| Adequate Liquidity | Current assets adequately cover current liabilities |

| No Statutory Defaults | No material tax arrears affecting solvency; statutory dues paid |

| Solvency Opinion | Entity is solvent for the last 2 years; not undergoing insolvency/liquidation/bankruptcy |

SECTION 08Frequently Asked Questions (FAQs)

📧 Email: emihelpdesk-dic@gov.in

📞 Phone: 011-23310014

You can use this for queries, feedback, complaints, or implementation difficulties.

Need Help Evaluating Your EMI Eligibility?

The EMI Scheme involves multiple eligibility criteria, document preparation, and a CA Solvency Certificate (with UDIN). Getting it right the first time matters.

Get in Touch with CA Kunal KapoorThis is an educational resource. Please consult a qualified professional before taking any action based on this content.